One of the things I’ve long thought about this country is that we’re not equipped for serious banking and should return to a cash economy or barter system. By serious banking I don’t mean complicated functions like regulating interest and exchange rates. I just mean a citizen’s daily dealings with the banking sector without which life would come to a halt: using an ATM, writing a check, making an online bank transfer, that sort of thing. For some reason, the most perfunctory of bank transactions trigger a chain reaction of security alerts to make you feel like a terrorist financier doing a heist.

I often don’t have cash on me and have to make online cash transfers to corner stores or the Habib tuck shop where I buy chips or those new Cadbury chocolate-filled biscuits you see everywhere these days. (They are really astoundingly good.) To log into my bank app, they send an OTP code to my email AND phone that expires in fifteen seconds. If by some miracle the code actually arrives on the 14th second and I punch it in, I’m reminded by phone AND email that I did it, I accessed my own account. Thank you, I did not know. Then, to add a new beneficiary and send money, a string of additional OTPs are sent at every step, and finally, a huffy phone and email message saying the money has left my account and there’s nothing I can do about it now. Why must I contend with twenty-five new phone messages and emails to send Rs. 150 to a shopkeeper? “Ma’am for your own security,” I’m told by one bank officer or another each time I complain.

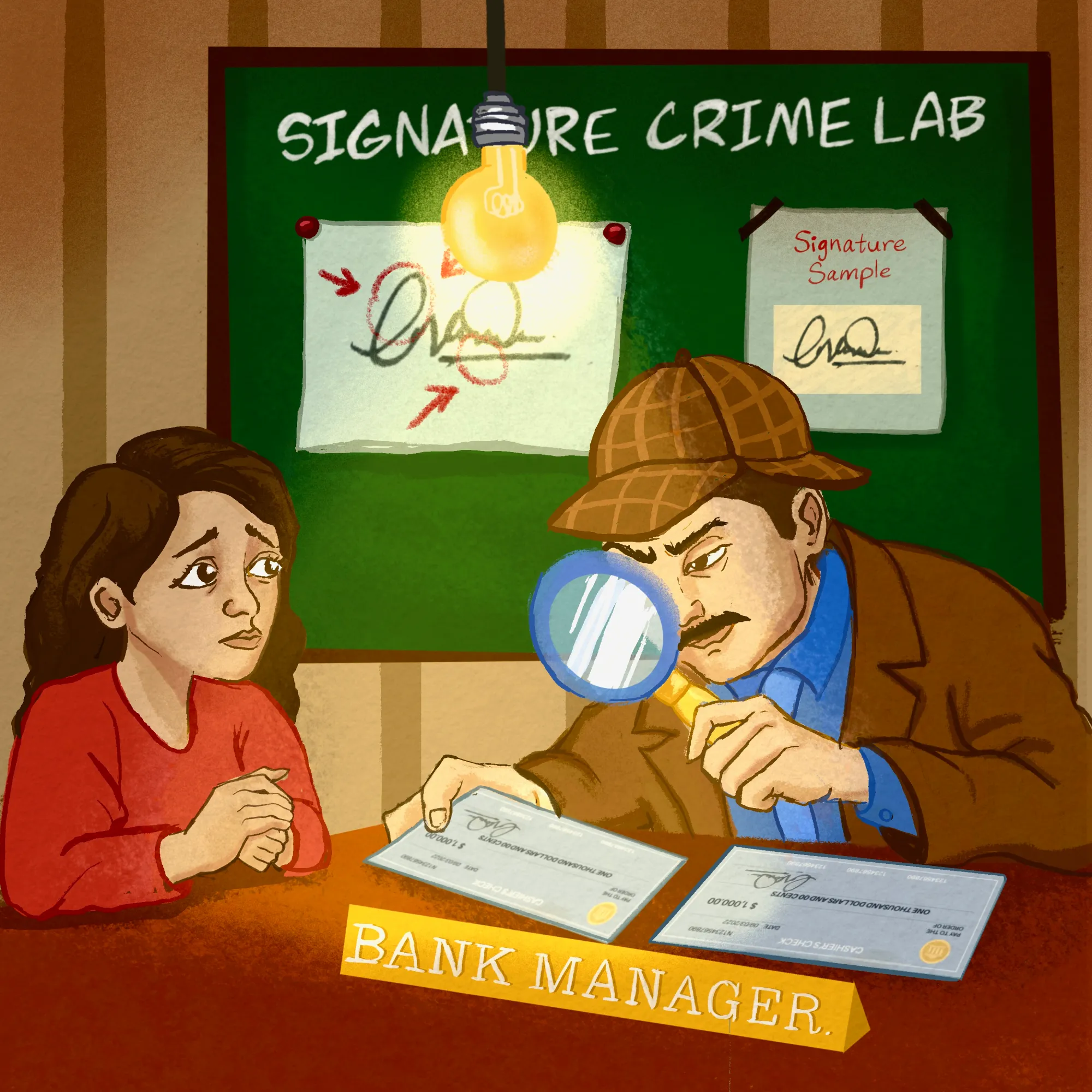

So exigent are the demands of security that banks even have processes in place to protect you from yourself. Once, I wrote a check and presented it to a bankteller. He stared at it a while and then asked for my CNIC, which he placed alongside the cheque and inspected with the hawk eyes of a jeweler staring at a zircon masquerading as a diamond. Finally, he looked up and said, “Ma’am the signature doesn’t match, I can’t cash this cheque.” Mystified, I emptied out my wallet and laid my cards on the counter to assure him that I was, in fact, the person I claimed to be: Jawziya Zaman, the owner of this face, this CNIC, this checkbook and debit card and credit card and driver’s license, all carrying the name belonging to me, Jawziya Zaman, the person standing in front of him. What else could I have said? He heard me out, his eyes brimming with the sorrowful patience of a judge listening to the final plea of a condemned prisoner. Then he pointed to my signature on the check and said, “Ma’am ‘Z’ ke loop ka masla hai.”

Why must I contend with twenty-five new phone messages and emails to send Rs. 150 to a shopkeeper? “Ma’am for your own security,” I’m told by one bank officer or another each time I complain.

On closer examination of the check I saw he was right: the ‘Z’ ka loop on my name was slanted compared to the magnificently rounded ‘Z’ ka loop on my CNIC. After a few failed attempts at copying my own signature to the bankteller’s satisfaction, he handed me a blank sheet of paper and suggested I practice before ruining the next check: “Sorry ma’am, security ke liye.”

It seemed easier to comply than to argue about the blinding absurdity of the situation, so I filled that blank sheet with my signature over and over again. But, as I learned that day, if the burden of proving your entire identity hangs on a loop, it is very likely that you’ll keep messing it up. Which I did. I messed it up so many times that the issue was finally escalated to a higher up. She studied the problem and turned to my sister, who’d accompanied me to the bank because boring errands are best undertaken with a sibling in tow. “Maybe you can try it?” she asked.

Apa just happens to be an excellent forger, so after a few tries, she got the signature, I got my money, and the bank upheld its commitment to combat fraudulent activity. Needless to say, I switched to another bank soon afterwards, one that friends assured me wouldn’t require jumping through such hoops (and loops).

I emptied out my wallet and laid my cards on the counter to assure him that I was, in fact, the person I claimed to be: Jawziya Zaman, the owner of this face, this CNIC, this checkbook and debit card and credit card and driver’s license, all carrying the name belonging to me, Jawziya Zaman, the person standing in front of him. What else could I have said?

There are no OTPs or emails at the new place and no one’s ever attacked my signature, but there are other obstacles. They’ve launched a much-lauded new phone banking app that routinely rejects my login info, refuses to read my fingerprints, and denies me facial recognition. On the rare days it lets me access my account, it won’t allow online transfers or renew my Zong monthly phone plan. I’ve been assigned to a banking officer but she is one of two women in the whole bank and understandably bored and under-stimulated. Every time I go to her for troubleshooting, she gives me tea and makes me analyze the before/after pictures from her weight loss journey over the years. I don’t have the heart to tell her that the before pictures are so much nicer. I know her gym schedule, her strength-training routine, her ideal jawline and fixation on sharp collar bones. “But the app is really awful,” I insist, “can’t you do something about it?” She looks up from her selfies and says, “Pata nahi yaar, mera app toh chal raha hai.” The banking officer on the next desk overhears the conversation and leans over to tell me that his app is useless and there’s no point lodging a complaint because the IT department is also useless. He turns back to his empty desk and she to her phone.

Do our banks actually want money to move? Is money safest when no one can touch it or reach it? Are sharp collarbones really all that? Honestly, who knows. There is nothing left to do but finish the tea and take leave, my mountain of biscuit-related debt intact and zero balance on my phone.

Jawziya Zaman is a writer, teacher, and academic editor.